Establishing a strong credit history can be a daunting task, but credit building apps offer a helping hand in navigating this complex terrain.

In this article, we explore the top credit building apps that simplify the process of building credit and improving financial well-being.

From monitoring credit scores and providing valuable education to budgeting tools and credit builder loans, these apps cater to a range of needs.

Additionally, we highlight the importance of credit monitoring and identity theft protection in maintaining a secure credit profile.

Join us as we delve into the world of credit building apps, equipping you with the knowledge to make informed choices and embark on a transformative financial journey.

How To Choose The Best Credit Building Apps

Choosing the best credit building app requires careful consideration of several factors. Here are some key considerations to help you make an informed decision:

Features and Functionality

Look for apps that offer the specific features you need, such as credit score monitoring, educational resources, budgeting tools, credit builder loans, or secured credit card options. Assess whether the app’s functionality aligns with your credit building goals.

User Interface and Experience

A user-friendly interface enhances your experience with the app. Consider apps with intuitive navigation, clear visuals, and easy-to-understand information. Read user reviews to gauge the overall user experience and satisfaction.

Security and Privacy

Ensure the app prioritizes the security and privacy of your personal and financial information. Look for apps that use encryption and have robust security measures in place. Check if they have a privacy policy detailing how they handle and protect your data.

Credibility and Reputation

Research the credibility and reputation of the app and the company behind it. Check for user reviews, ratings, and feedback from reputable sources. Look for established financial institutions or companies with a track record in the industry.

Cost and Value

Consider the cost of using the app. Some apps offer free basic features with the option to upgrade for advanced functionalities at a cost. Evaluate whether the benefits and value provided by the app justify the cost.

Customer Support

Good customer support is essential when using any financial app. Check if the app offers reliable customer support channels, such as email, chat, or phone support, to address any concerns or issues promptly.

Integration and Accessibility

If you already use other financial tools or apps, consider whether the credit building app can integrate with your existing systems. Additionally, assess the app’s availability on different platforms (mobile, web) to ensure it suits your preferred devices.

What Are The Best Credit Building Apps?

Below are some of the best credit building apps to try this year:

- Self

- Kikoff

- Credit Builder Card

- Credit Strong

- Moneylion

- SeedFi

- Brigit

- StellarFi

- Experian

- Sable

- Credit Sesame

1. Self

Best Overall Credit Building App

Self is a standout credit building app that offers a distinct and effective approach to improving credit scores and building financial stability. What sets Self apart from other credit building apps is its innovative credit builder loan feature and commitment to customer empowerment. Self stands as a compelling choice for individuals seeking a comprehensive credit building solution.

Self’s primary offering is its credit builder loan, which allows users to build credit by making small monthly payments into a secure certificate of deposit (CD). As users make these payments, Self reports the positive payment activity to major credit bureaus, gradually building a positive credit history. This method offers a tangible and structured way to establish credit, making Self an attractive option for those starting from scratch or looking to rebuild credit.

Over 4,500,000 people have signed up with Self to build credit, and the platform has received a high satisfaction rating of 4.7 stars based on over 1,031 reviews from actual customers.

Self Key Features:

- Credit Builder Account: Self provides a Credit Builder Account that allows customers to build credit history with three leading credit bureaus. By making on-time payments, customers can see an average credit score increase of 49 points*.

- Two Ways to Build Credit: Self offers two options for building credit. Customers can choose to build credit by saving, where they save money while building their credit. Alternatively, they can pay rent and utilities to build credit based on their existing monthly payments.

- No Hard Pull: When applying for a Self Credit Builder Account, there is no hard pull on your credit, ensuring that your credit score is not negatively affected during the application process.

- Reporting to Credit Bureaus: Every on-time monthly payment made by customers is reported to all three credit bureaus, helping them establish a positive payment history.

- Self Visa Credit Card: Customers who have a Credit Builder Account can gain access to the Self Visa Credit Card in as little as three months*. This card provides additional opportunities to build credit responsibly.

- Transparent Pricing: Self offers four credit builder plans tailored to different goals and budgets. Each plan comes with a specific monthly payment, administrative fee, total payments, and final cost.

- Trust and Security: Self prioritizes security and uses 256-bit AES encryption. They are a SOC 1 type 2 compliant organization, ensuring the safety of customers’ personal and financial information.

Self Pros & Cons:

Pros of Self:

- Unique Credit Builder Loan

- Financial Education

- Alternative Credit Assessment

- Credit Monitoring

- Personalized Credit Improvement Recommendations

- Empowers Individuals

- Inclusive Approach

- Structured and Tangible Method

- Transparency and Customer Support

Cons of Self:

- Monthly Payments Required

- Membership Fee

Self Pricing:

Self offers four credit builder plans with different pricing options.

- Small Builder: Monthly Payment: of $25

- Medium Builder: Monthly Payment of $35

- Large Builder: Monthly Payment of $48

- X-Large Builder: Monthly Payment of $150

These plans offer different payment amounts, durations, and potential returns. The specific plan you choose will depend on your budget, goals, and financial situation.

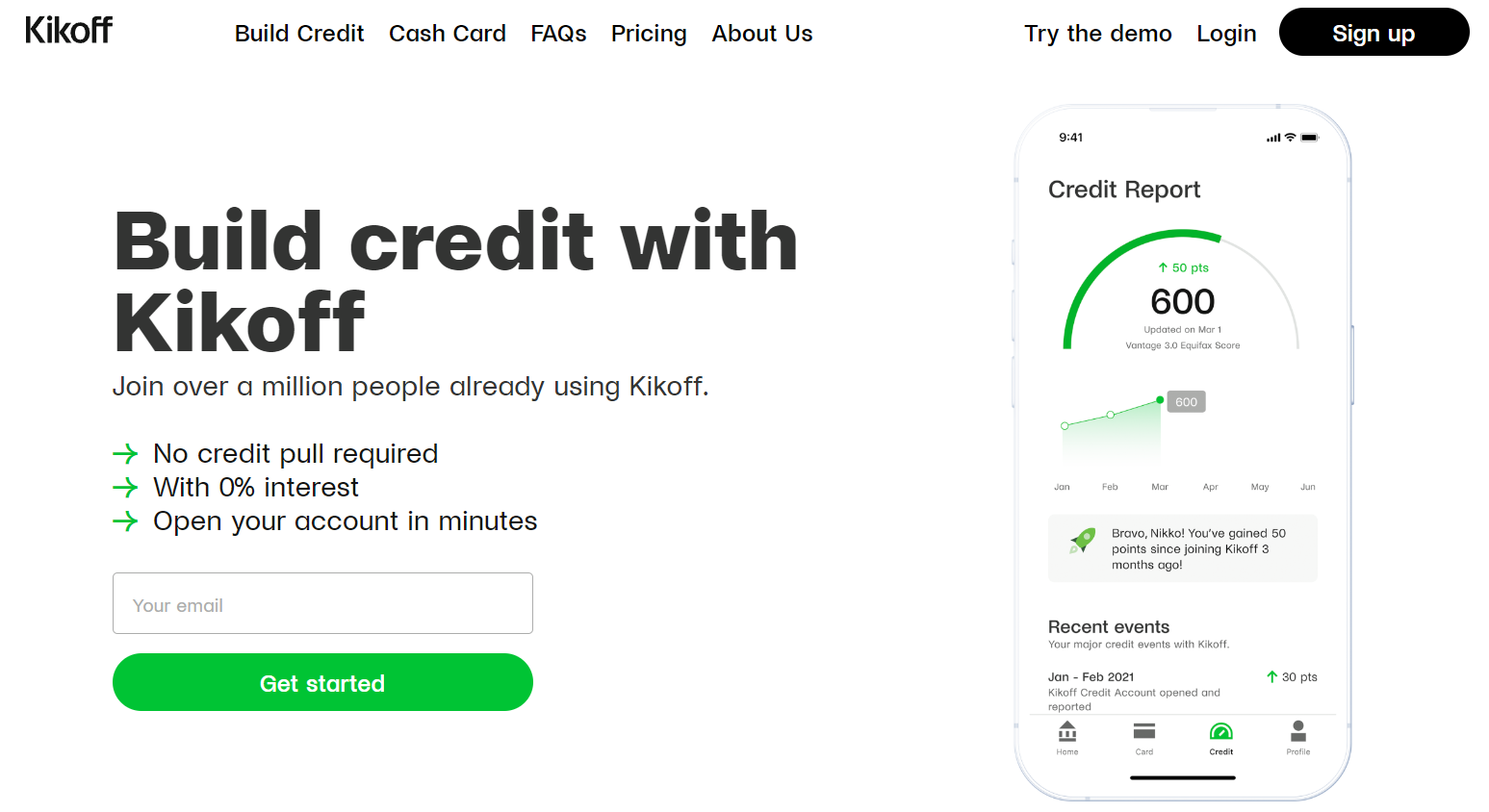

2. Kikoff

With over a million users, Kikoff offers various products to assist users in improving their credit scores. The primary product is the Kikoff Credit Account, which is a revolving line of credit designed to address key credit score factors such as payment history, credit utilization, and age of accounts. By using the Credit Account to finance purchases from Kikoff, users can make monthly payments without interest or fees, and Kikoff reports these payments to Equifax and Experian.

One of the key advantages of Kikoff is that it does not require a credit check or hard pull, making it accessible to individuals with no credit or low credit. The service starts at $5 per month and offers easy and automatic payments with the optional Autopay feature. Kikoff provides credit monitoring reports, allowing users to track their credit journey and gain insights into problem areas.

Kikoff Key Features:

- Cash Card: Kikoff provides the Credit+ Cash Card, a secured credit card on the Mastercard network. This card functions like a checking account and debit card, allowing users to make everyday transactions while building their payment history.

- No Credit Pull Required: Kikoff does not require a credit check or hard pull when signing up. This means users can start building credit without worrying about negative impacts on their credit scores.

- 0% Interest: With Kikoff, users benefit from 0% interest on their Credit Account and Credit Builder Loan. This allows them to focus on building credit without incurring additional costs.

- Easy and Automatic Payments: Kikoff offers the option of Autopay, ensuring that users never miss a payment. This feature simplifies the payment process and helps users maintain a positive payment history.

- Credit Monitoring Reports: Kikoff provides credit monitoring reports that allow users to track their credit journey. These reports offer insights into problem areas and help users stay on track to increase their credit scores.

- Official Data Furnisher: Kikoff is an official data furnisher to the three major credit bureaus – Equifax, Experian, and TransUnion. This ensures that users’ credit activities and progress are reported to these bureaus, helping to establish a positive credit history.

Kikoff Pros & Cons

Pros:

- Mobile app available

- No impact on your credit score when you sign up

- You can continue paying even after you have paid off your loan

- Helps with credit utilization

- Get a $500 line of credit

Cons:

- You have to use their products in order to improve your credit score

- Isn’t the best to save money since the loan amount is small

Remember to consider these points in the context of your specific needs and circumstances.

Kikoff Pricing:

Kikoff provides customers with two pricing options tailored to their specific needs.

The first option is the Credit Monthly Membership, available at a cost of $2 per month. With this membership, users gain access to a $500 line of credit and the convenience of an online dashboard.

The second option is the Credit Builder Loan, which offers a more advantageous solution compared to the monthly service fee. Despite the loan amount being small, this choice can be highly beneficial for individuals seeking to gradually improve their credit score over time.

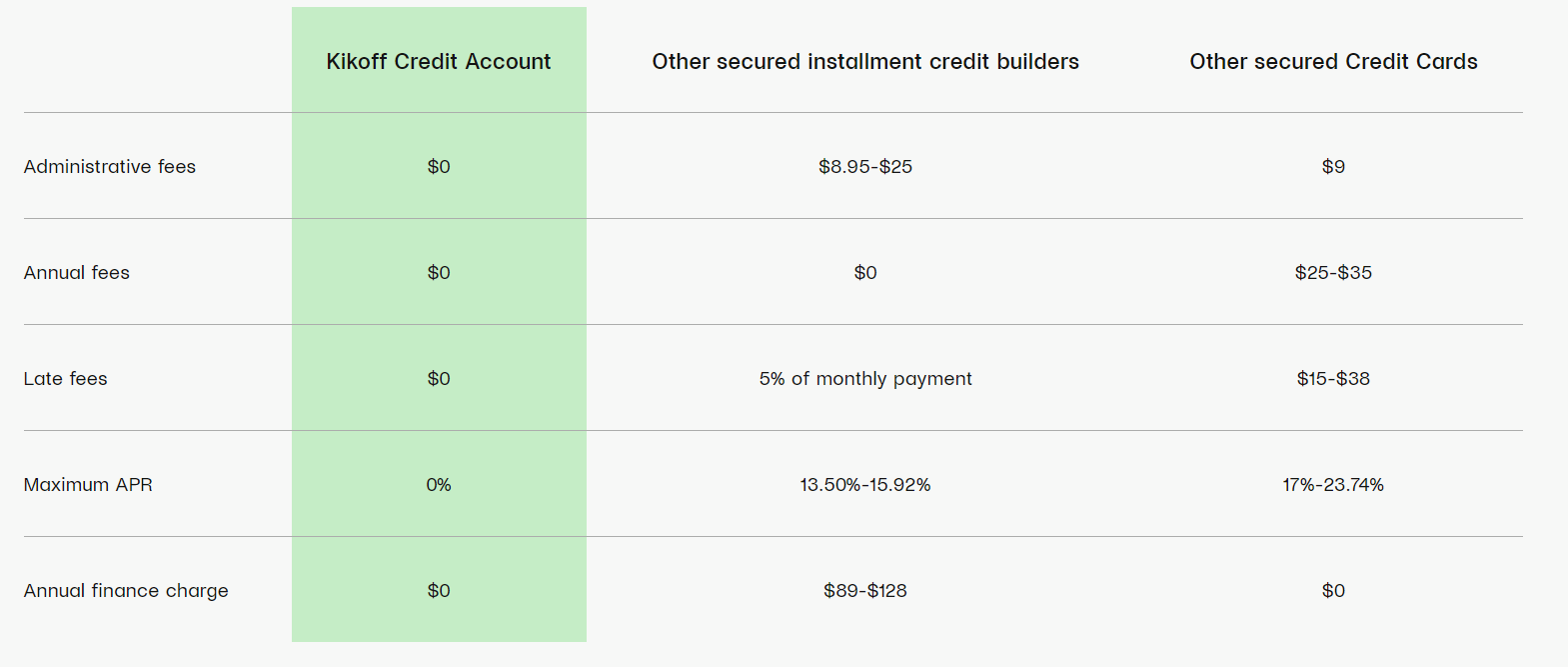

3. CreditStrong

Credit Strong offers two main products: Credit Builder Loans and Credit Strong for Small Business. With a Credit Builder Loan, customers can borrow a specific amount of money, typically ranging from $1,000 to $2,500, and make fixed monthly payments over a predetermined term, usually 12 to 24 months.

The borrowed funds are held in a savings account as collateral, which earns interest and can be accessed once the loan is fully paid off. By making timely payments, customers can demonstrate responsible credit behavior and potentially improve their credit scores.

Credit Strong for Small Business works similarly but is designed for entrepreneurs and small business owners who want to establish credit for their businesses. The loan proceeds are held in a business savings account, and timely payments are reported to business credit bureaus.

CreditStrong Key Products:

- Revolv: Instantly build revolving credit without requiring a monthly payment. This option can help improve credit utilization, a crucial factor in credit scoring.

- Instal: Build installment credit and savings simultaneously with a low fixed monthly payment on a Credit Strong credit builder loan. Multiple plans are available to suit individual preferences.

- CS Max: For individuals with the means but limited credit, CS Max offers the largest and longest credit builder accounts in the nation. It helps build significant credit history and can be used for personal or small business credit building.

CreditStrong Pros & Cons

Pros of Credit Strong:

- Multiple credit-building options, including revolving credit and installment credit.

- Plans tailored to personal and small business credit-building needs.

- No hard credit pull when opening an account.

- Educational resources and support to help customers understand credit-related topics.

- The potential to improve credit scores through responsible credit behavior.

- Availability of customer support to address inquiries and concerns.

- Large and long credit builder accounts available through CS Max.

- Positive testimonials from satisfied customers.

Cons of Credit Strong:

- Fees and interest rates associated with credit builder loans.

- Not a credit repair service and cannot remove negative credit history.

- Credit profile improvement is not guaranteed.

- Failure to make timely payments may negatively impact credit profiles.

- Limited information on specific interest rates and fees on the website.

- Limited flexibility in loan terms and repayment options.

- Limited information on the approval process and eligibility criteria.

- Lack of specific details on the impact of their services on credit scores.

CreditStrong Pricing:

Here are the pricing details for Credit Strong:

Subscription Plan:

You have the option to choose between two subscription plans:

- $15 per month

- $30 per month

These plans include credit report monitoring and access to their online dashboard, providing you with valuable insights into your credit.

For as low as $15 per month, you can build credit with a $1,000 installment account. This plan allows you to customize your payment terms, with options available for up to 120 months. You also have the flexibility to cancel your subscription at any time.

Build and Save Plan:

The Build and Save plan offers three pricing options to choose from:

- $38 per month

- $48 per month

- $96 per month

By selecting one of these options, you can work towards building a good credit history while potentially saving up to $2,000 by the end of your selected term.

4. Credit Builder Card

Credit Builder Card offers a fantastic solution for individuals seeking to enhance their FICO scores. By utilizing this secured credit card, you can unlock the potential for significant credit improvement.

Join the ranks of over 100,000 satisfied customers who have harnessed the power of Credit Builder Card to boost their credit scores. With their innovative approach, you can leave behind the risks associated with high-interest credit cards.

Here’s how Credit Builder Card works:

- Simple and Secure Deposit: To get started, you deposit $200, which serves as collateral and determines your credit limit. This process ensures that you have control over your credit usage while mitigating risk for the card issuer.

- Seamless Usage: Once your deposit is made, you can begin using your Credit Builder Card just like any other credit card. This means you can make purchases online and offline, pay bills, and enjoy the convenience of a credit card in your day-to-day transactions.

- Monthly Reporting to Major Credit Bureaus: The real power of Credit Builder Card lies in its commitment to report your credit activity to all three major credit bureaus each month. This consistent reporting provides an opportunity to demonstrate your responsible credit management, leading to faster credit building.

- Rapid Credit Growth: With each monthly report, your positive payment history and responsible credit usage will be reflected in your credit reports. As a result, you can witness the gradual improvement of your FICO scores over time. This is an effective way to establish or rebuild your creditworthiness.

- Deposit Return and Card Cancellation: The exciting aspect of Credit Builder Card is that once you have successfully built up your credit, you can reclaim your deposit and cancel the card if you wish. This ensures that you not only improve your credit but also have the flexibility to move on to unsecured credit options in the future.

Credit Builder Card Pricing:

Getting started with Credit Builder Card is a breeze, and all you need is a $200 security deposit. Here’s what you can expect in terms of pricing and benefits:

- Deposit Determines Credit Limit: Your credit limit will match your deposit amount. By depositing $200, you will have a credit limit of $200. This straightforward approach ensures a clear understanding of your available credit.

- Convenient Online Payments: Managing your payments is simple and hassle-free with Credit Builder Card. Enjoy the convenience of making payments online, allowing you to stay on top of your finances with ease.

- No Annual Fee: Credit Builder Card is designed to be cost-effective. You won’t have to worry about any annual fees, keeping your expenses in check while you focus on building your credit.

- Fast and Inclusive Approval Process: The application process is quick, taking just a few minutes of your time. Even if you have a less-than-perfect credit score, you can still apply and have a chance to be approved. Credit Builder Card believes in providing opportunities for individuals looking to improve their credit standing.

5. Experian

For consumers, the Experian credit building app provides access to free credit reports and scores from Experian, allowing users to monitor their credit health. It offers credit advice and guidance on improving credit scores, along with information on credit cards, loans, and auto financing. Users can also explore topics such as identity theft, fraud protection, and the latest scams to stay informed and safeguard their personal information.

Small businesses can benefit from the app by accessing credit-building resources tailored to their needs. They can learn about establishing credit, obtaining business loans, and protecting their financial interests. The credit building app offers insights into factors that impact creditworthiness and provides access to tools such as credit card payoff calculators and personal loan calculators.

Businesses can leverage the app to gain a better understanding of credit-related matters. They can explore topics such as liability insurance, car insurance, and credit card options. The app provides information on credit approval odds for auto loans and rental applications.

The Experian Credit Builder app follows a step-by-step process to guide users towards building credit. It encourages users to enroll in a free membership and offers personalized credit-building strategies. Users are provided with educational resources, including e-books, to enhance their credit knowledge. The app also offers credit monitoring, 3-bureau reports, and FICO® Scores.

In terms of usability, the app is available for download on both the Apple App Store and Google Play. Users can access support for freezing their credit file, disputing information on their credit reports, and receiving assistance in case of identity theft. Experian’s commitment to diversity, equity, and inclusion, as well as data privacy, is highlighted.

Experian Pros & Cons:

Pros:

- The Experian Credit Builder app is free to use, making it accessible to a wide range of users.

- It allows users to include common bills like rent in their credit history, potentially boosting their credit score.

- Users can access their free Experian credit score through the app, providing them with valuable insights into their credit health.

Cons:

- The impact on your credit score may vary, and depending on the number of payments reported, the app may not lead to a significant difference in your score.

Experian Pricing:

The app is free to use.

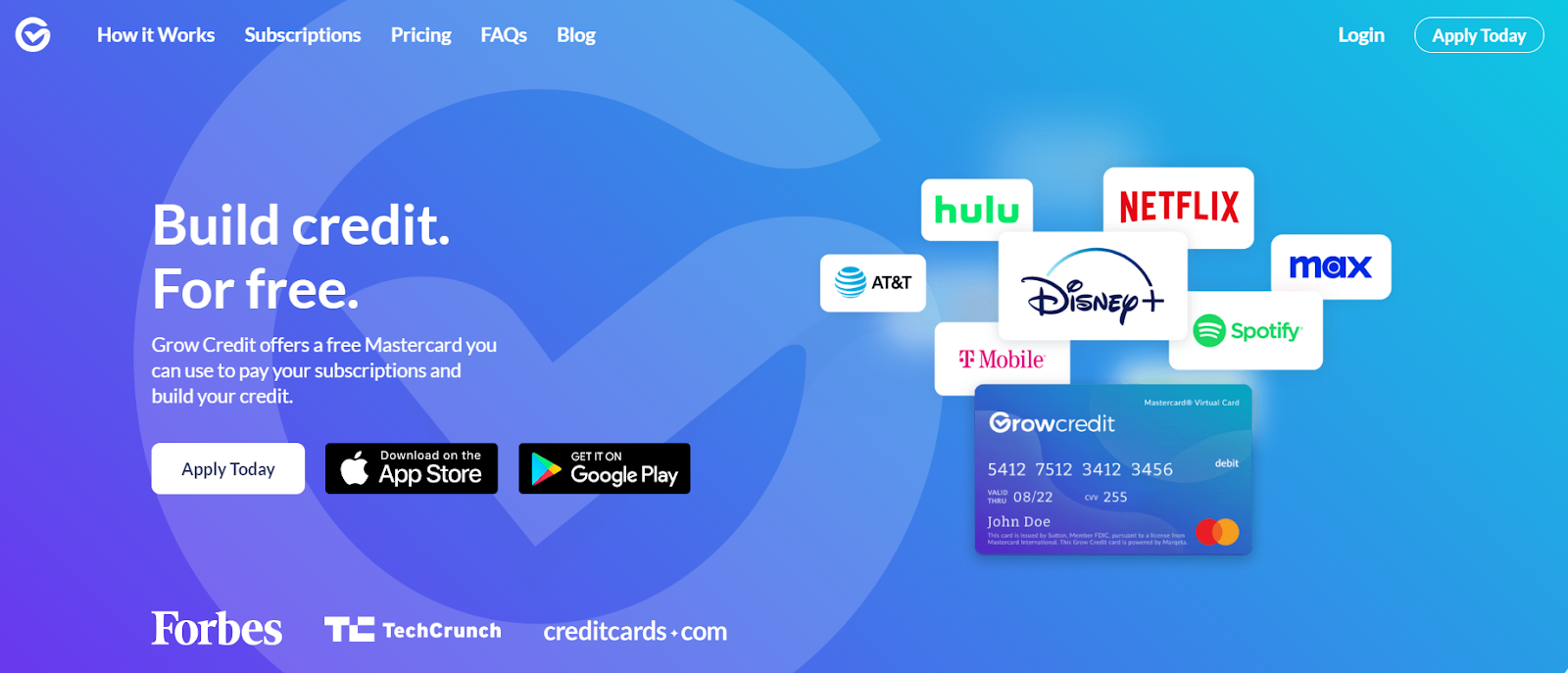

6. Grow Credit

Grow Credit is a free MasterCard that offers a unique and innovative approach to help individuals improve their credit scores significantly. By leveraging regular recurring expenses, users can build credit without having to spend any extra money. The card can be used to pay for a wide range of subscriptions, including popular services like Netflix, Disney+, Hulu, HBO, as well as essential bills such as Wi-Fi and phone bills.

With Grow Credit, users have the opportunity to enhance their credit history and credit mix by demonstrating responsible financial behavior through timely payments for their existing subscriptions. This approach provides an alternative credit-building method for individuals who may have limited or no credit history and may not have access to traditional credit-building tools such as credit cards or loans.

One of the significant advantages of Grow Credit is that it enables users to utilize their regular expenses, which they would have already incurred, to contribute positively towards their credit score. By using the Grow Credit MasterCard, individuals can establish a track record of timely payments, showcasing their financial responsibility and creditworthiness.

By offering a seamless and convenient way to build credit, Grow Credit aims to empower individuals, particularly younger individuals or those with limited credit history, to take control of their financial future. It provides a viable option for individuals who want to build credit and improve their credit scores while leveraging their existing subscription expenses.

Grow Credit Pros & Cons:

Pros:

- Enables significant improvement in credit history and credit mix.

- Provides a free virtual MasterCard specifically designed for regular recurring subscriptions.

- Potential to see an increase in credit scores within 60-90 days of enrollment.

- Functions effectively as a revolving line of credit.

Cons:

- Some users have reported issues with app logouts during usage.

- The monthly spending limit is relatively limited.

- Paid plans require a security deposit.

- Only one bank account can be added for withdrawals.

Grow Credit Pricing:

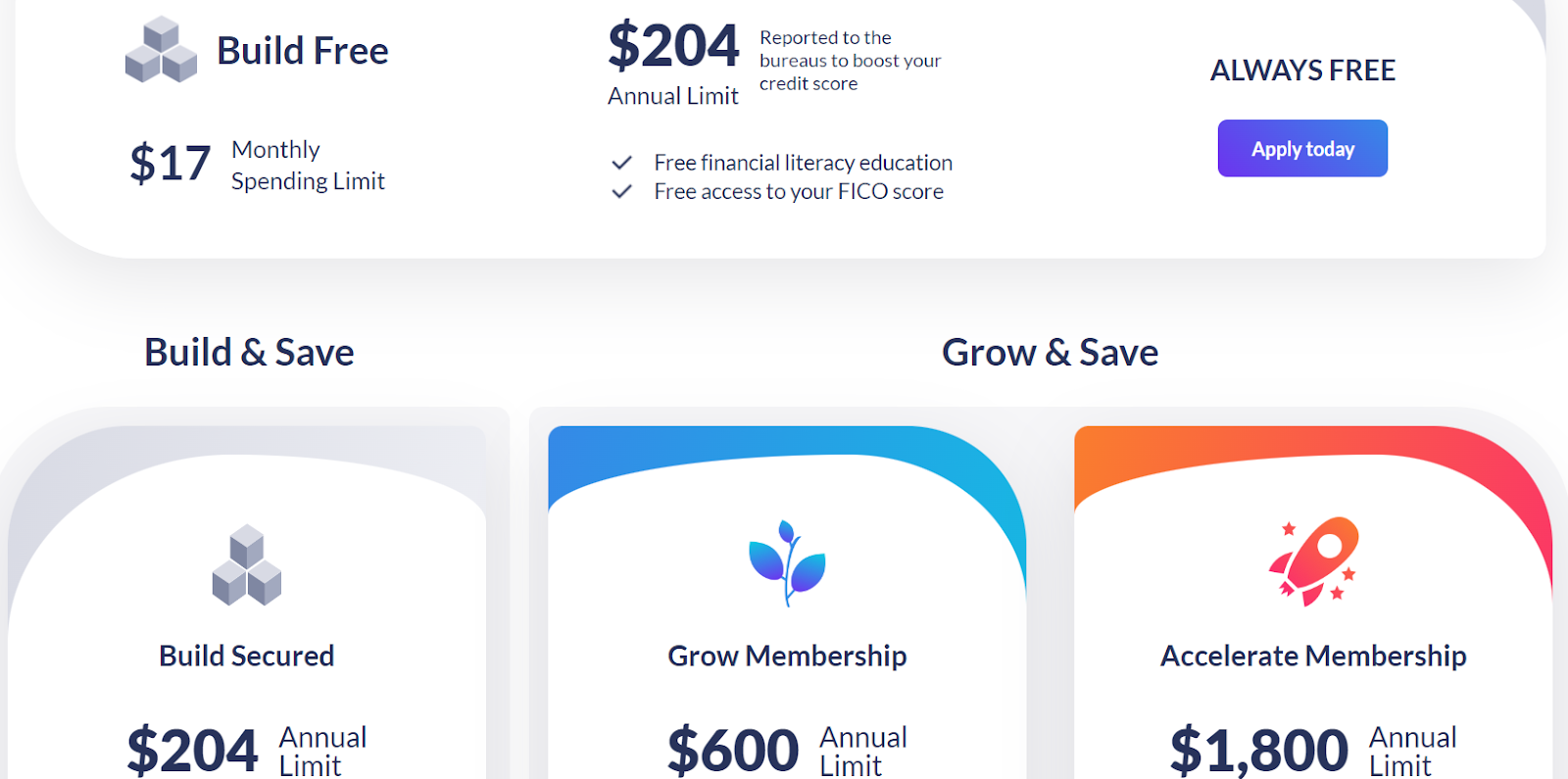

Grow Credit offers a range of pricing plans, allowing users to choose the one that suits their needs. The Build plan is free and provides a monthly spending limit of $17. Users have the flexibility to upgrade to a paid account whenever they desire.

One of the standout features is that Grow Credit reports to Equifax, Experian, and TransUnion, which can greatly benefit users in building their credit history. Additionally, users can enjoy complimentary FICO score updates and access to free financial education classes.

Here are the pricing plans offered by Grow Credit:

- Build Free: This plan has a monthly spending limit of $17 and is always free for users.

- Build Secure: Users with this plan also have a $17 monthly limit but become eligible to upgrade after making six monthly payments. The plan starts at $1.99 per month.

- Grow & Save: This plan offers a higher monthly spending limit ranging from $50 to $150. It starts at $3.99 per month.

If you have a poor credit history but regularly subscribe to services like Netflix or other recurring subscriptions, Grow Credit can be one of the best tools to build credit and pave the way for a more secure financial future.

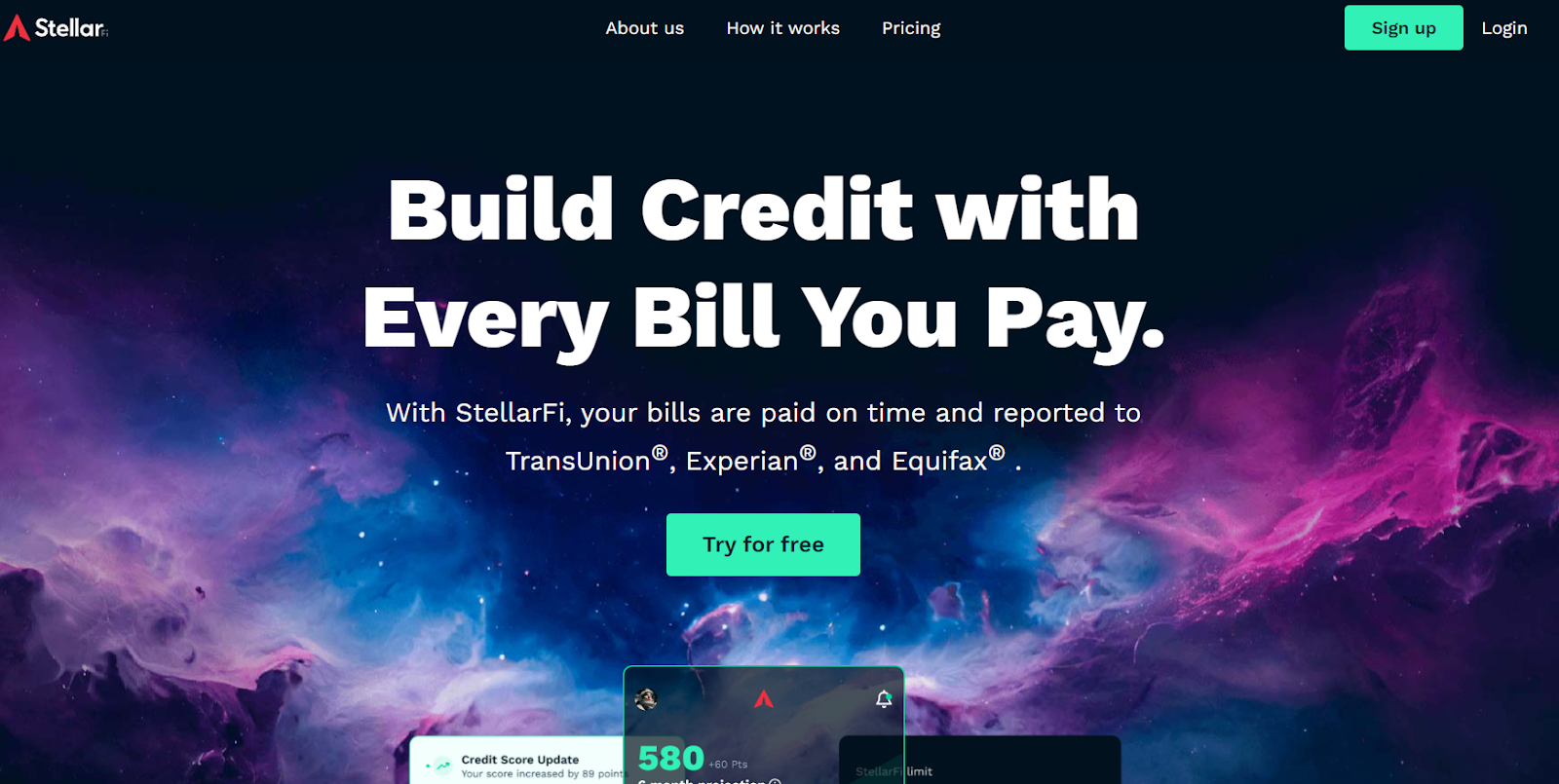

7. StellarFi

StellarFi is an innovative credit-building application designed to enhance your credit while tracking your monthly subscriptions. By simply linking your StellarFi bill pay card, you can ensure timely payments for all your subscriptions.

In addition to facilitating on-time payments, StellarFi offers a user-friendly online dashboard that enables you to effortlessly monitor your bills and payment history. Moreover, they provide complimentary credit monitoring services, empowering you to stay updated on your credit status at no cost.

StellarFi Pros & Cons:

Pros:

- Assists in the improvement of a negative credit history.

- Enables the creation of personalized credit-building objectives.

- Offers one-on-one credit consulting services.

- Reports credit activity to major credit bureaus such as Experian, Equifax, and TransUnion.

- Provides identity protection through their premium plan.

- Facilitates automatic payments for convenience.

- Monitors credit scores effectively.

- Ensures transparency with no hidden fees.

Cons:

- Requires continued payment to observe future credit improvements.

StellarFi Pricing:

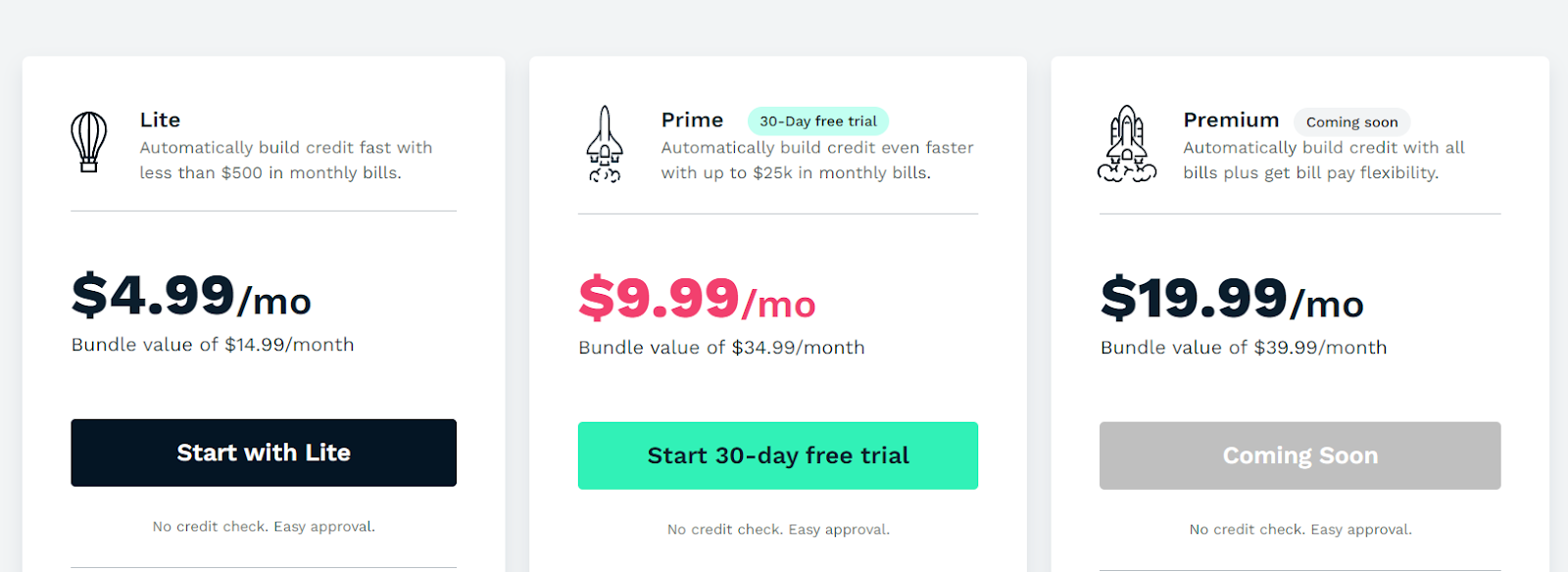

StellarFi’s credit builder app offers budget-friendly plans suitable for everyone looking to get started. Their plans are available at a range of prices, starting from $4.99 and going up to $19.99, each offering distinct tiers of features.

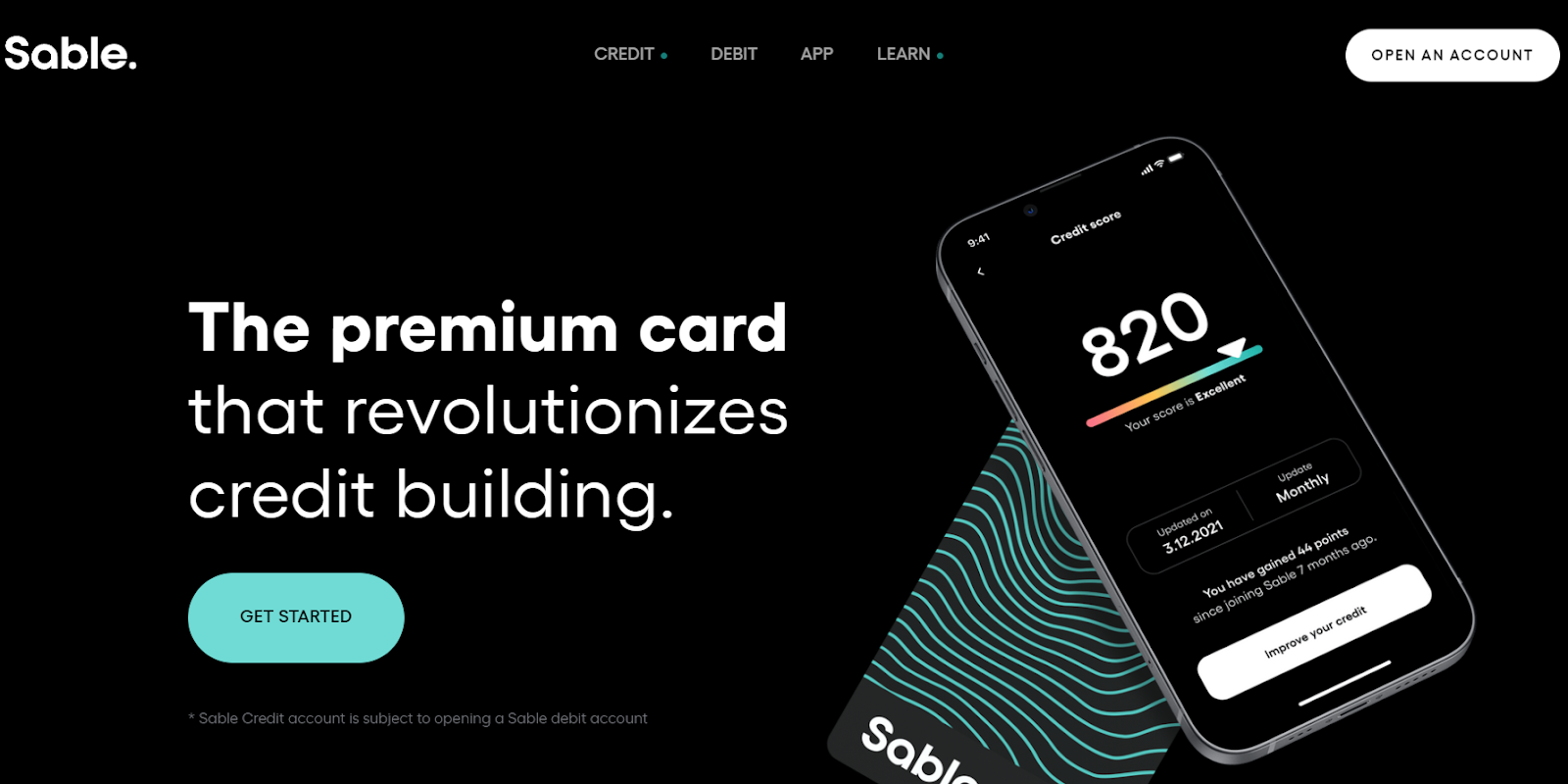

8. Sable

If you are seeking a way to enhance your creditworthiness while avoiding the risk of accumulating debt then look no more, because Sable One Credit is here to help.

Sable One Credit is a secured credit card that provides you with the opportunity to transition to an unsecured card after making on-time payments for four months. Unlike conventional credit cards, which often burden you with exorbitant interest fees and mounting debt, Sable Credit offers unlimited cash back on all your purchases. This feature makes it an excellent option for individuals aiming to enhance their financial status.

Furthermore, the user-friendly Sable app simplifies the management of your account like never before. If you’re ready to elevate your credit to the next level, there’s no need to search any further than Sable Credit. It’s the intelligent choice for prudent spending.

Sable Pros & Cons:

Pros:

- Convenient setup of autopay for timely monthly payments

- No annual fees

- Access to premium card perks

- Notifications from Credit Report Bureaus

- Simple process for freezing your account

- No soft or hard credit inquiries

- Availability of a debit card with cash back rewards

Cons:

- Online reviews indicate that customer support may not be the strongest aspect of the service.

Sable Pricing:

To get started, you are required to make an initial deposit, which will determine your credit limit.

Your credit limit will match the amount of your deposit. For example, if you deposit $300, your credit limit will also be $300.

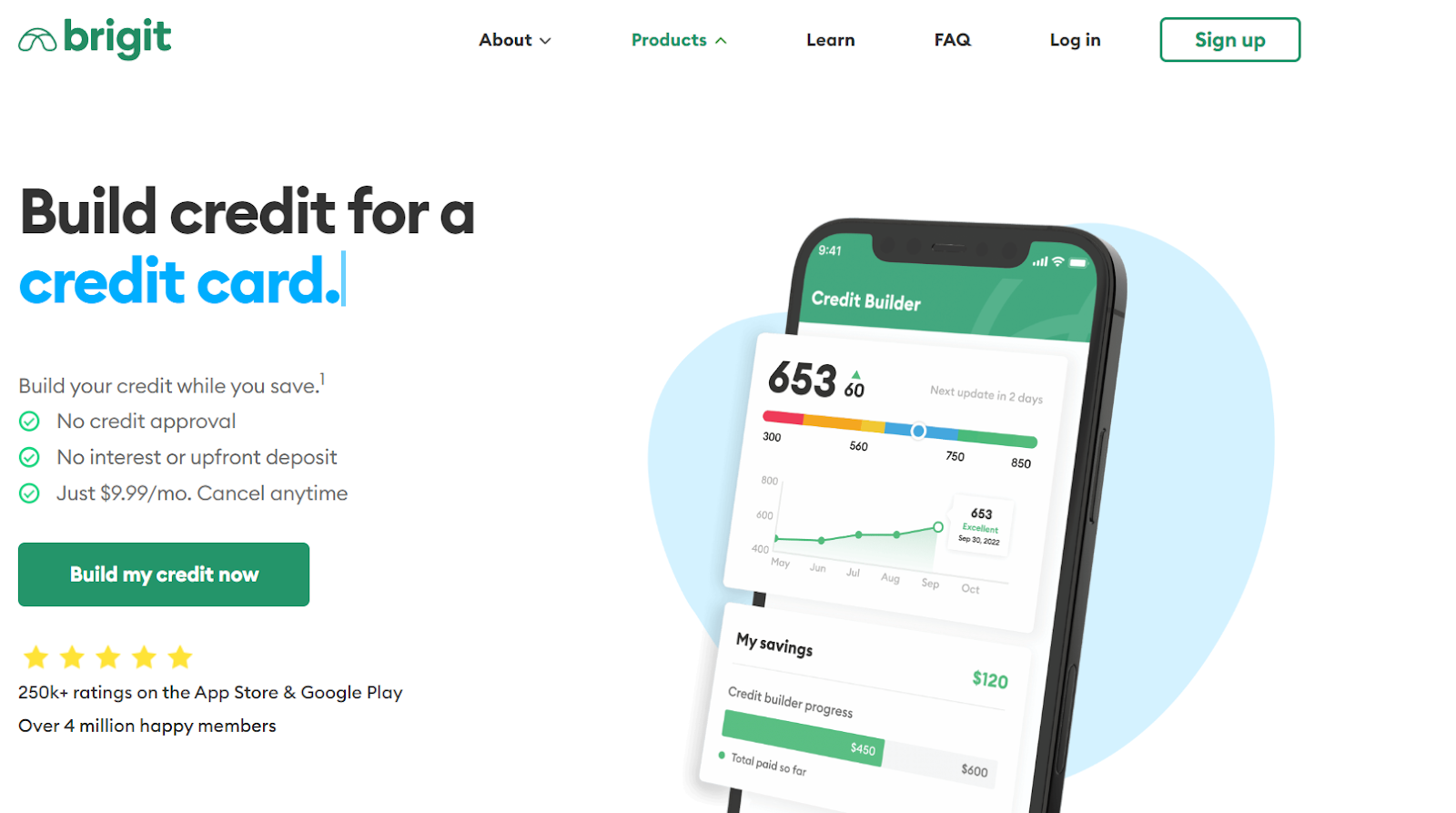

9. Brigit

Brigit Credit Building app helps individuals build credit while saving money.

With instant approval and no credit check, users can start building credit in seconds.

By contributing as little as $1 a month, users establish positive payment history, which is reported to major credit bureaus.

After 24 months, the loan is paid off, and users have improved credit and access to their savings.

Backed by Ashton Kutcher and Kevin Durant, Brigit Credit Building has garnered over 4 million happy members and 250k+ ratings on the App Store and Google Play, making it a trusted and effective credit-building tool.

Brigit Key Features:

- No credit approval required: Brigit Credit Building offers instant approval, making it accessible to individuals with no or bad credit.

- No interest or upfront deposit: Users do not have to worry about paying upfront fees, deposits, or interest.

- Affordable monthly fee: Brigit Credit Building charges a monthly fee of $9.99, providing an affordable option for credit building.

- Positive payment history: On-time payments are reported to the three major credit bureaus, helping users establish a positive payment history, a critical factor in credit scores.

Brigit Pros & Cons:

Pros:

- Instant approval for credit building account.

- No credit check required.

- Affordable monthly fee of $9.99.

- No upfront deposit or interest charges.

- Positive payment history reported to major credit bureaus.

- Option to contribute as little as $1 towards savings.

- Over 4 million happy members and 250k+ ratings on App Store and Google Play.

Cons:

- Limited customer support options available.

- App-specific limitations or technical issues could affect user experience.

Brigit Pricing:

The Brigit Plus membership provides access to the credit building features, including the Credit Builder account and savings options. Users can enjoy the benefits of building their credit while also having the opportunity to save money.

10. Kovo

Kovo is a credit-building app and a registered Public Benefit Corporation that aims to empower consumers in taking control of their finances.

Unlike traditional loans, Kovo’s credit-building approach involves providing customers access to a range of self-help courses on finance and entrepreneurship.

These courses are purchased on credit, and customers pay them off over a period of 24 months.

By participating in these courses and making on-time payments, customers can establish a positive payment history with major credit bureaus, potentially boosting their credit scores.

Kovo reports payment information to TransUnion, Experian, Equifax, and Innovis. The app also offers rewards on loans, charges 0% APR, and does not require a credit check.

Kovo Key Features:

- No credit check: Kovo does not require a credit check when signing up, making it accessible to individuals with limited or poor credit history.

- Access to self-help courses: Kovo offers a wide range of interactive courses designed to improve financial literacy, business skills, and overall personal development. These courses cover topics such as job interview skills, entrepreneurship, personal branding, stress management, and more.

- Rewards and loan offers: After making four on-time payments, users become eligible for loan offers, including personal loans, student loans, student loan refinancing, and credit cards. Kovo provides gift cards as rewards for taking out featured loans, offering additional incentives for credit improvement.

- Credit bureau reporting: Kovo reports payment information to TransUnion, Equifax, Experian, and Innovis, ensuring that users’ on-time payments are reflected in their credit reports.

- No APR or prepayment penalties: Kovo does not charge an annual percentage rate (APR) on its credit builder program. Additionally, there are no prepayment penalties, allowing users to pay off their loans early without incurring extra charges.

- FICO score access: Users gain access to their FICO credit scores, enabling them to monitor their credit progress over time.

Kovo Pricing:

Kovo credit building app operates on the following pricing structure:

- Cost: The total cost of accessing the self-help courses on Kovo is $240.

- Payment Terms: Users make monthly payments of $10 over a period of 24 months to complete the payment for accessing the courses.

11. MoneyLion

MoneyLion is a financial technology company that offers a range of services and products to help individuals improve their financial well-being. The company provides an app called Credit Builder Plus, which focuses on helping users build credit while also offering various other features and benefits.

MoneyLion Key Features:

- Credit Builder Loan: MoneyLion’s Credit Builder Plus program offers users a loan that helps them establish a positive credit history by making on-time payments. A portion of the loan funds is made available upfront, providing immediate access to funds.

- Credit Monitoring: Users can monitor their credit score and key credit factors, such as credit utilization, through the app. This feature allows individuals to track their progress and make informed decisions regarding their credit.

- Personalized Insights: MoneyLion provides users with personalized credit-building insights and tips sent directly to their inbox. These insights can help individuals make better financial decisions and improve their credit behavior.

- 0% APR Instacash: The app offers the option to access cash advances of up to $300 per pay period with no interest charges (0% APR). This feature helps users cover their everyday expenses without resorting to costly alternatives.

- RoarMoney and MoneyLion Investment Account: MoneyLion encourages users to open a RoarMoney℠ or MoneyLion Investment account, offering benefits such as waived account fees and the opportunity to earn cashback rewards through the app.

MoneyLion Pricing:

MoneyLion offers a membership program called Credit Builder Plus, which provides access to various features and benefits. The membership cost is $19.99 per month.

What Are Credit Building Apps?

Credit building apps are mobile applications or online platforms designed to assist individuals in improving their credit scores and overall creditworthiness. These apps provide various tools, features, and resources to help users establish, monitor, and manage their credit profiles effectively. Credit building apps typically offer services such as:

- Credit Score Monitoring: They allow users to regularly monitor their credit scores and receive updates on any changes or fluctuations.

- Credit Education: They provide educational resources, tips, and insights to help users understand credit scores, credit reports, and credit management techniques.

- Budgeting and Expense Tracking: Some credit building apps include budgeting tools that assist users in managing their finances, tracking expenses, and avoiding late payments.

- Credit Improvement Recommendations: These apps may offer personalized recommendations and strategies for improving credit scores based on individual credit profiles.

- Credit Builder Loans: Some credit building apps provide access to credit builder loans, which are specifically designed to help individuals build positive credit history through regular payments.

- Secured Credit Cards: Certain apps facilitate the process of obtaining secured credit cards, which can be used to build or rebuild credit by making responsible purchases and timely payments.

- Credit Monitoring and Identity Theft Protection: Credit building apps may offer features for monitoring credit reports and protecting against identity theft or fraudulent activities.

Credit building apps aim to empower individuals by providing them with the knowledge, tools, and opportunities to establish and improve their creditworthiness. By leveraging these apps, users can take proactive steps towards achieving their financial goals and accessing better credit options in the future.

Alternative Ways To Build Credit

There are various methods to build credit apart from credit building apps. Some alternative ways to establish and improve credit include:

Secured Credit Cards

Secured credit cards require a security deposit as collateral, allowing individuals with limited or poor credit history to demonstrate responsible credit usage. By making timely payments, users can gradually build positive credit history.

Credit-Builder Loans

Credit-builder loans, offered by some financial institutions, allow individuals to borrow a small amount of money. The borrowed funds are typically held in a savings account or certificate of deposit (CD) as collateral. Regular payments towards the loan help establish a positive payment history.

Become an Authorized User

Becoming an authorized user on someone else’s credit card allows you to benefit from their positive credit history. Ensure that the primary cardholder has a strong payment history and low credit utilization to maximize the impact on your credit score.

Peer-to-Peer Lending

Peer-to-peer lending platforms connect borrowers directly with individual lenders. Successfully repaying a peer-to-peer loan can help build credit history over time.

Rental Payments Reporting

Some services allow rental payment data to be reported to credit bureaus. Consistently paying rent on time can contribute positively to your credit profile.

Credit Builder Accounts

Some financial institutions offer credit builder accounts, where individuals make monthly payments into a savings account. Once the account is paid in full, the funds become available to the account holder.

Responsible Credit Usage

Utilize credit responsibly by making timely payments and keeping credit card balances low. Avoid maxing out credit cards or applying for multiple credit accounts simultaneously.

Remember, building credit takes time and consistency. It’s important to use any credit-building method responsibly and maintain good financial habits to gradually improve your creditworthiness.

Frequently Asked Questions

How do credit building apps work?

Credit building apps typically work by connecting to your financial accounts and analyzing your financial behavior. They evaluate factors that contribute to your credit score, such as payment history, credit utilization, and length of credit history. Based on this information, these apps provide personalized recommendations to improve your creditworthiness.

What features do credit building apps offer?

Credit building apps may offer various features, including:

Credit score monitoring: Regular updates on your credit score and credit reports.

Financial education: Resources and tips to help you understand credit and improve your financial habits.

Credit analysis: Evaluation of your credit profile, identifying areas for improvement.

Budgeting and spending tracking: Tools to help you manage your finances and stay on top of your payments.

Credit-building strategies: Tailored suggestions to improve your credit score, such as paying bills on time or reducing credit utilization.

Credit-builder loans: Some apps may offer credit-builder loans, where you make monthly payments that are reported to credit bureaus, helping you establish a positive credit history.

Identity theft protection: Monitoring for potential identity theft or fraud.

Are credit building apps safe to use?

Credit building apps can be safe to use, but it’s important to choose reputable and well-established apps with strong security measures. Look for apps that use encryption to protect your personal and financial data and have clear privacy policies. Additionally, read user reviews and check if the app has been subject to any security breaches in the past.

Do credit building apps guarantee an increase in my credit score?

Credit building apps can provide guidance and tools to help you improve your credit score, but they cannot guarantee specific results. Ultimately, your credit score depends on your financial behavior, such as making timely payments, maintaining low credit utilization, and managing your debts responsibly. The app’s recommendations and features can assist you in achieving those goals.

Are credit building apps free?

Some credit building apps offer basic services for free, but they may also have premium or subscription-based features that require payment. The availability of free and paid features varies among different apps. It’s important to review the pricing structure of the app you’re considering to understand what features are included for free and which ones require a fee.

Can credit building apps help people with no credit history?

Yes, credit building apps can be particularly helpful for individuals with limited or no credit history. These apps often provide strategies and tools to establish a credit history, such as credit-builder loans or secured credit cards. By using these services responsibly, individuals can begin building a positive credit history.

Can credit building apps repair bad credit?

Credit building apps can guide individuals with bad credit by offering strategies to improve their credit scores over time. They may suggest actions like paying off delinquent accounts, disputing inaccuracies on credit reports, or creating a budget to manage debts effectively. However, credit repair is a gradual process, and it requires consistent effort and responsible financial behavior.

Last updated on July 7th, 2023 at 09:37 am

Pingback: How To Start A Credit Repair Business In 2023: Ultimate Guide - ES Group Digital

Pingback: How To Become A Credit Repair Specialist in 2023: The Ultimate Guide - ES Group Digital

Pingback: A Beginner's Guide to Credit Repair Software - ES Group Digital

Pingback: Six Tips for Healthy Tech Gadgets Gear Gadgets and Gizmos

Pingback: KOVO Credit Builder Review 2023: Is It Worth It? [UPDATED]